In the previous post Comparing Walkability in the Mid-Valley, grocery access within walking distance was established as a primary limiting factor in the walkability of Mid-Willamette Valley cities. Albany was identified as having fewer grocery stores overall than the two most comparable communities analyzed, Corvallis and Springfield, both of which also fared significantly better on the same walkability analysis.

The next phase of this analysis will attempt to identify specific ways in which Albany differs from other comparable communities in terms of grocery access.

First, a brief overview of the retailer categories used in this analysis:

| Category | Description | Example Stores/Brands |

| Warehouse Club | Large, member only wholesale clubs offering grocery and other items in bulk at discounted prices. | Costco, Sam’s Club |

| Super Store | Stores offering many departments and a wide variety of goods, of which grocery may or may not be the primary focus. | Fred Meyer, Target, WalMart |

| Supermarket | Traditional grocery supermarkets primarily focused on a variety of grocery and food products. | Safeway, Albertsons, Roth’s, Market of Choice, WalMart Neighborhood Market, IGA, WinCo |

| Small Format/Specialty | Grocery retailers offering a limited number of SKUs, typically in lower square footage facilities. | Grocery Outlet, Aldi, Trader Joe’s, specialty grocers, small independent grocers |

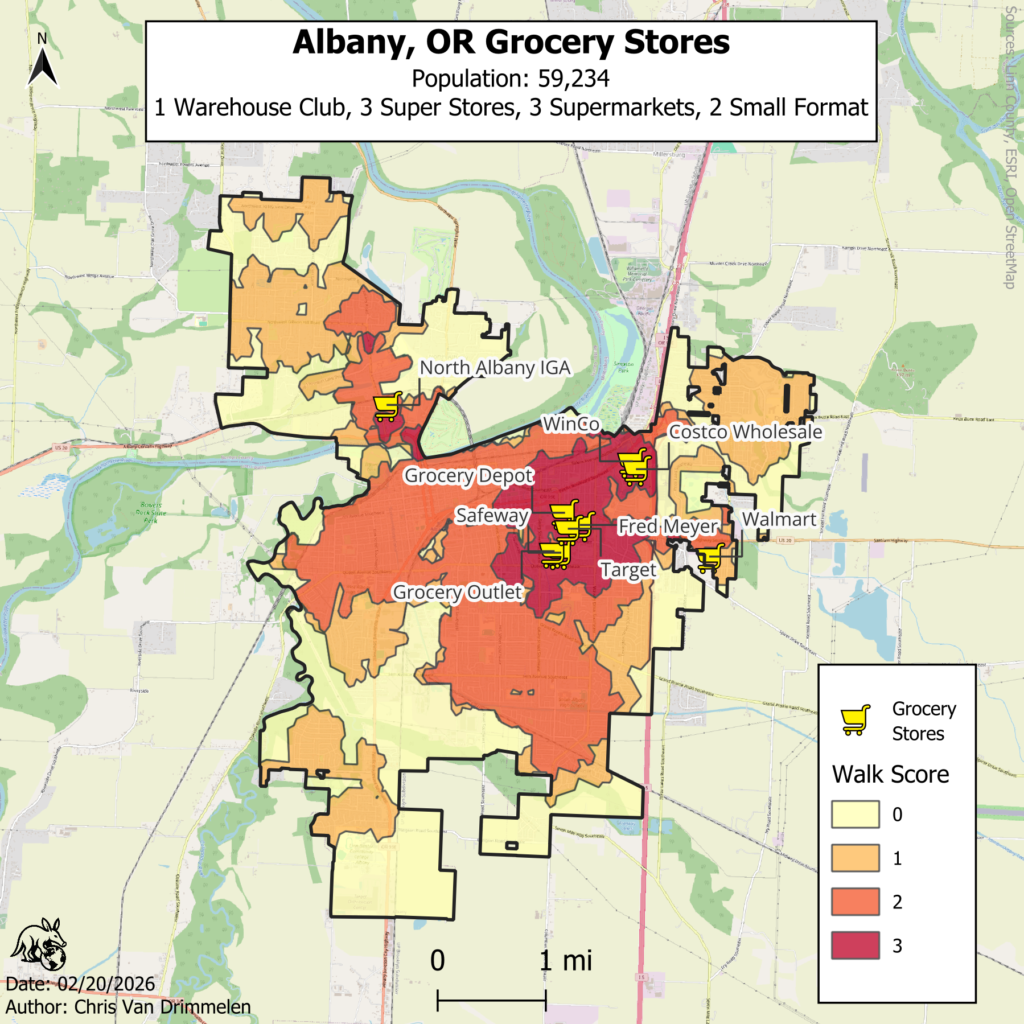

This map from the previous post breaks down which grocery retailers operate in Albany and where. The tight spatial clustering of most grocery retailers on its face creates inequitable access throughout the city. While each retailer has a different business model meant to address a specific segment of the grocery market, it would be fair to say that even if the number of grocery stores in Albany did not increase, but the businesses themselves were more spread out, this would alleviate at least part of the issue.

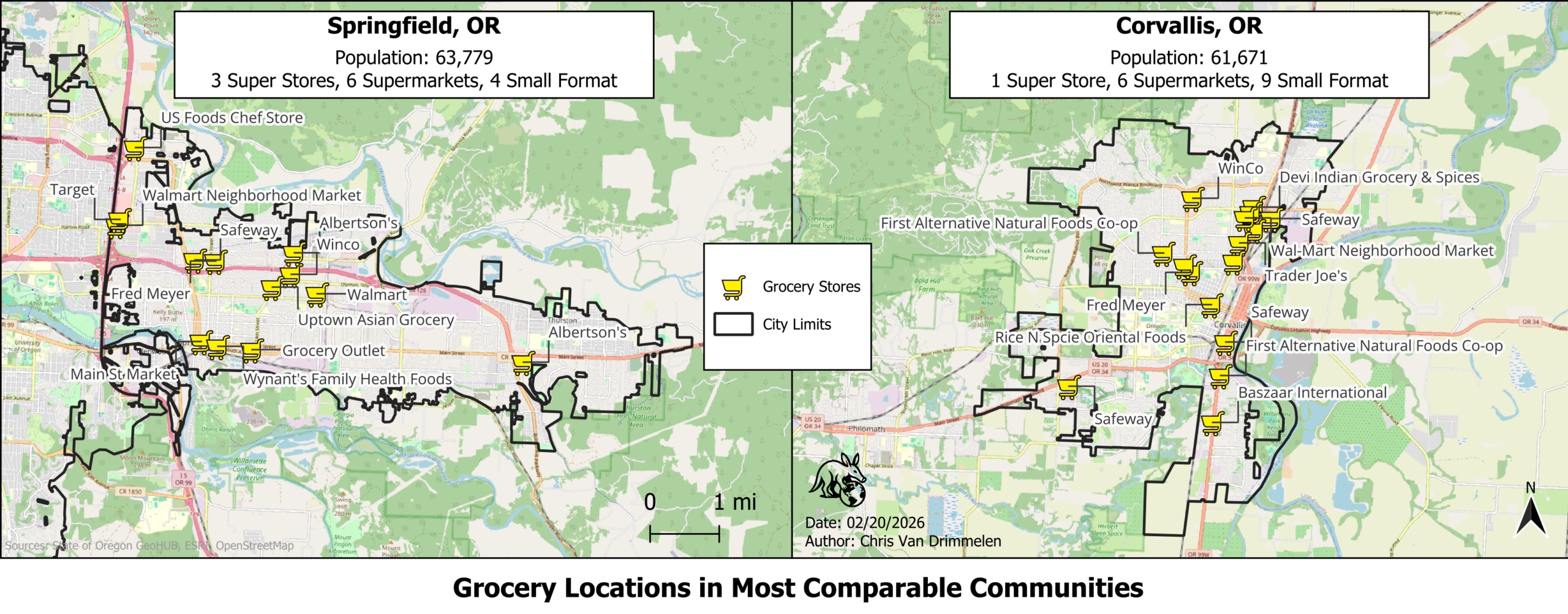

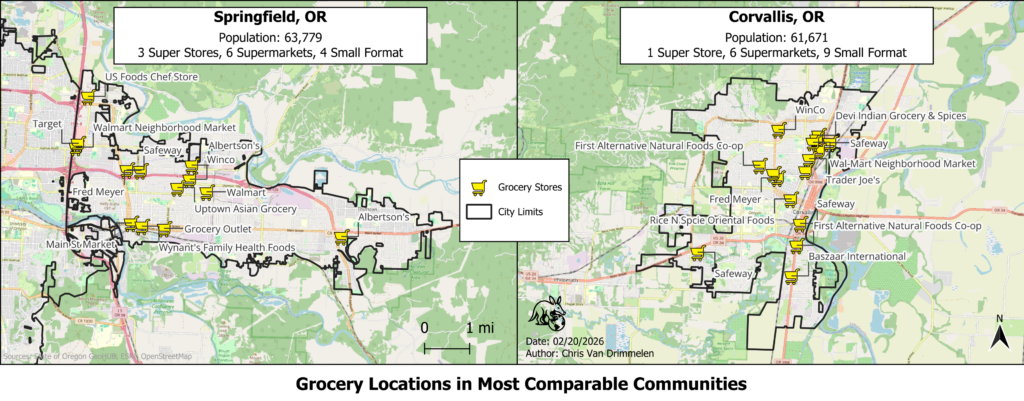

We did, however, see in the last post that both Corvallis and Springfield have a greater overall number of grocery stores within their city limits, possibly indicating that Albany is in fact underserved in the grocery market, and that additional stores might be part of a potential solution (which is a more realistic scenario than relocation of already established retailers).

Taking the two most comparable communities and mapping grocery retailers throughout the city, we can see that while some spatial clustering of stores exists, it is not nearly so pronounced as in Albany. Initial observations of which retailers operate in these cities also reveals a greater variety of store types than Albany has, particularly in the small format and specialty category (shortened to just “small format” for the map subtitles). Major takeaways include:

- Both Springfield and Corvallis have a higher raw number of grocery stores than Albany, 13 and 16 respectively to Albany’s 9.

- Both comparator communities have at least double the number of small format and specialty grocery retailers, and small format retailers in these cities fill different niches in the market, such as natural or ethnic foods in addition to traditional grocery. Albany has only 2 small format grocery retailers: Grocery Outlet and Grocery Depot, both of which fill a similar, “discount/overstock” niche.

- Both communities seem to merit at least one national/regional brand operating multiple stores within the city limits. Of particular note is the fact that Albertsons Companies, Inc., owner of both the Safeway and Albertsons brands, operates three stores each in Corvallis and Springfield, while only maintaining one location in Albany.

It is important to note that while Springfield falls within the same general population range as Albany and Corvallis, it lies directly to the east of Eugene, a city of over 180,000 people, which likely has significant effects upon Springfield’s market (for example, Springfield lacks a Costco of its own, but Springfield residents are located relatively close to the one in Eugene). It is telling, however, that even with this much larger population just on the other side of I-5, retailers do not seem to expect that Springfield’s residents will simply go to Eugene for groceries – far from it, as Springfield has 13 grocery stores to Albany’s 9.

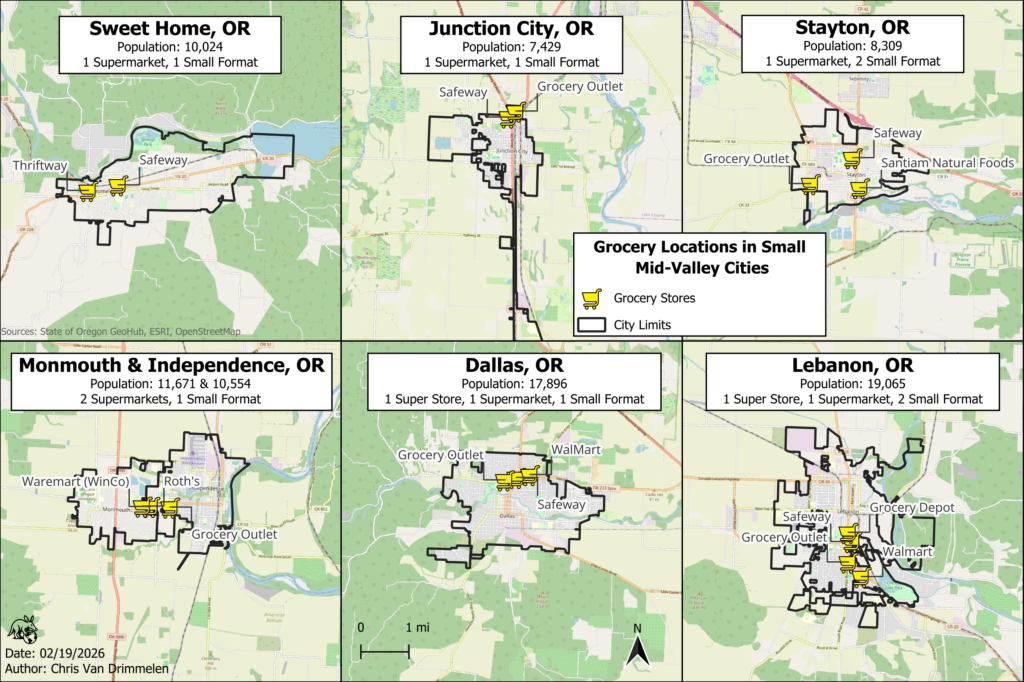

It may also be useful to compare grocery access in smaller mid-valley communities to establish a lower baseline, or “floor” for what to expect based on populations lower than that of Albany:

Smaller mid-valley cities with at least one grocery store were selected for comparison, resulting in a group of six communities ranging from almost 7,500 residents to nearly 20,000. In order of population from smallest to largest: Junction City, Stayton, Sweet Home, Dallas, Lebanon, and Monmouth/Independence (which while 2 cities was treated as a unit based on direct adjacency of the two communities).

Across these selected small cities, there does appear to be a rough trend where the smallest have a single traditional supermarket (generally Safeway), and an additional small format grocer, and as population increases, so does grocery access, either in the form of an additional supermarket in the case of Monmouth/Independence or the addition of a super store as with Dallas and Lebanon.

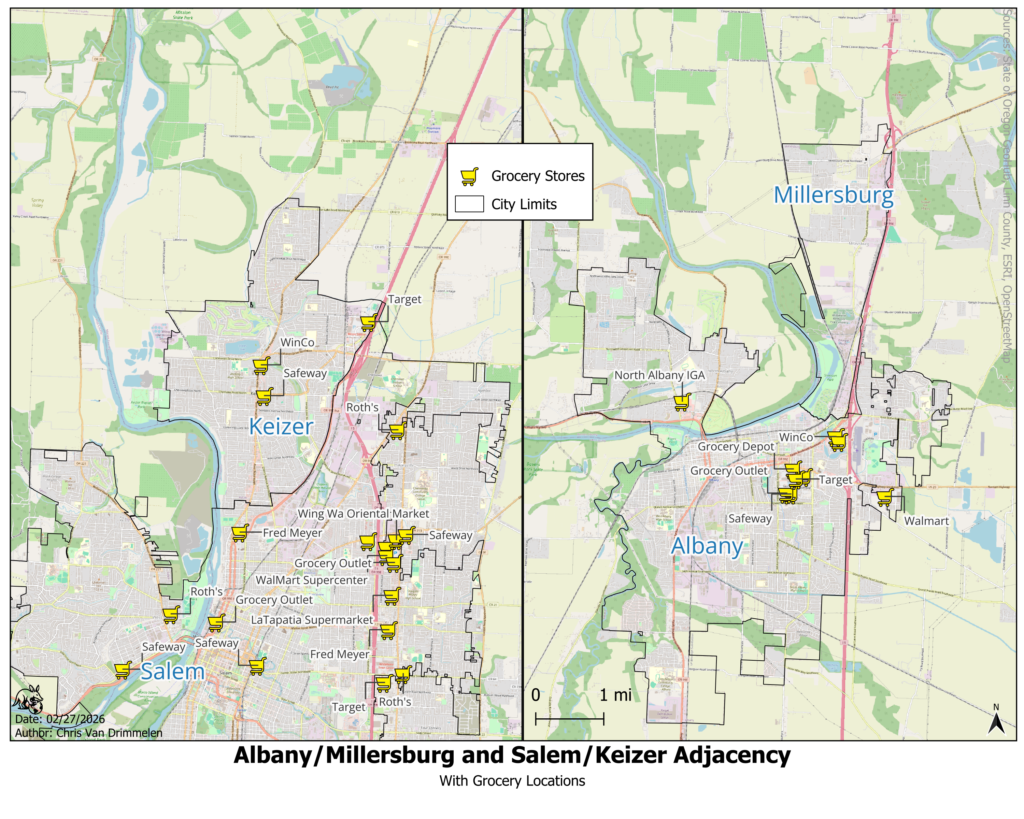

There are few communities that occupy the middle space between a community of about 20,000 like Lebanon and nearly 60,000 like Albany that also share the same kind of regional similarity to continue to build this trend with, with Keizer being an exception at about 40,000 people. Keizer is also, however, difficult to analyze in this context for similar reasons that Springfield merits a caveat above: Keizer is directly adjacent to Salem, another city of over 180,000 people. Technically, Keizer has only 3 grocery stores within its city limits, which lines up with significantly smaller communities like Stayton, Monmouth/Independence, and Dallas, with Lebanon even exceeding Keizer’s number of grocery retailers. This is, however, an incomplete picture when one considers that two Salem grocery stores, a Roth’s and a Fred Meyer, both sit less than a mile from the Keizer city limits, near enough that the North Salem Fred Meyer in particular even contributes to Keizer’s walk score (see previous posts) at the extreme southern limit of the city. This additional consideration puts Keizer more firmly on the trend that we see above where more residents equals more grocery access, with two super stores and three supermarkets.

Based on the caveats above, we would also be remiss to neglect the fact that Albany also directly borders the city of Millersburg in a similar manner to Eugene/Springfield and Salem/Keizer. According to Portland State University’s Population Research Center, Millersburg had a 2025 estimated population of 3,214. Millersburg also has no grocery stores of its own, so its customer base could rightly be considered to combine with Albany on this specific topic. This raises additional questions as to why the combined population of well over 62,000 people is served in a manner inconsistent with similar communities.

Coming soon: Evaluation of existing retailer practices. Who might fill the need?